Another option to raise funds to implement the recommendations in Patterson Park’s Master Plan is through charitable corporate giving. Typically, corporations give charitable donations to parks in three major ways: (1) direct giving; (2) through taxes imposed by a business interest district and (3) through sponsorships of events. With respect to the Patterson Park area, a business interest district does not exist. This leaves direct giving and sponsorships as potential sources of corporate giving.

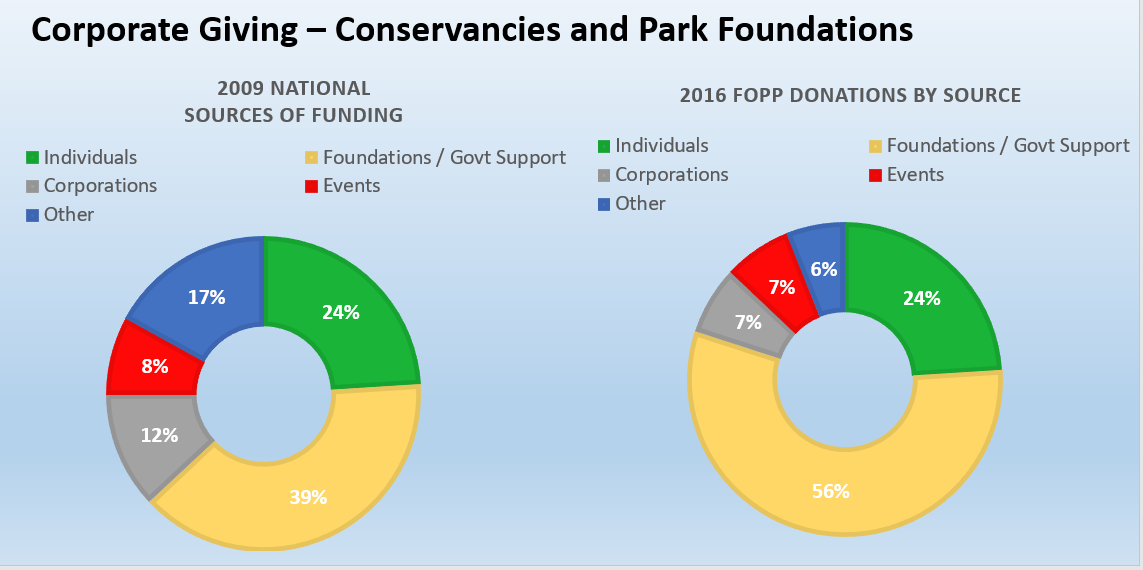

In the past, corporations have sponsored events and contributed to the Friends of Patterson Park through direct giving. Despite that fact, corporate contributions are only a small percentage of the charitable gifts received to support Patterson Park. For instance, the Friends of Patterson Park’s fundraising efforts for fiscal year 2016 indicate that only 7% of its total income came from businesses while 80% derived from foundation and government grants and individuals. The remaining 13% of funds derived from fundraising events and a small endowment. While the income derived from corporate giving is important, the Friends of Patterson Park’s fundraising experience suggest that corporate giving will only make up a small amount of the total fundraising income.

These numbers loosely match with corporate giving statistics nationwide. For instance, Giving USA estimates that businesses only made up 5% of charitable giving in 2016, while individuals and foundations constituted 87% of overall philanthropy.[1] Only about one-third of all companies claim charitable gifts on their federal corporate income tax returns.[2] With respect to parks, a small survey of seventeen conservancies and urban park advocacy organizations in 2009 indicated that corporations made up only 12.45% of park funding.[3] While the survey author makes clear that because of the small survey size, use of this survey should be done carefully, such numbers are in-line with the Friends of Patterson Park’s fundraising efforts. Such statistics suggest that corporate giving will only make up a small part of overall charitable donations to park systems.

Regardless of the amount of corporate giving, the location of Patterson Park serves as an additional obstacle to increasing corporate gifts. Patterson Park is surrounded by residential neighborhoods with some small businesses scattered among the rowhouses. There is not a concentration of large businesses. The absence of a concentration of businesses near the park is a disadvantage to receiving corporate donations. Although Patterson Park only has a few small businesses scattered throughout the neighborhoods surrounding the park, just a few miles away there is a concentration of large businesses. Many of those large corporations are contained within business interest districts that operate in the neighborhoods where they are located. In particular, the Downtown Partnership and the Waterfront Partnership manage two of the business interest districts nearest to Patterson Park.[4] Those business interest districts pool resources from the companies within their district to manage, maintain and promote the areas where they are located. Those pooled resources are used, in part, to maintain several parks within business interest district boundaries.

While some of those same businesses do contribute to Patterson Park, they are already otherwise obligated to fund maintenance and operations of the parks within their own district. Asking them to expand those obligations to a park outside of their district would be a tough sell. In addition, due to the lack of businesses near Patterson Park, creation of a business interest district is not feasible.

The Friends of Patterson Park’s experience along with national statistics suggest that corporate giving is not a reliable source of income to help fund the recommendations made in Patterson Park’s Master Plan. While improvements can always be made to corporate fundraising campaigns, it is not likely to yield sufficient results to improve spending at Patterson Park.

[1] Giving USA, Highlights: An overview of giving in 2016 (2017).

[2] Adrian Sargeant et. al, Fundraising Principles and Practice 434 (2010).

[3] Margaret Walls, Resources for the Future. Private Funding of Public Parks, Assessing the Role of Philanthropy 8-9, (2014) http://www.rff.org/files/sharepoint/WorkImages/Download/RFF-IB-14-01.pdf

[4] Downtown Partnership, http://www.godowntownbaltimore.com/about/dma-board/index.aspx Waterfront Partnership, Annual Report (2017), http://baltimorewaterfront.com/wp-content/uploads/2017/12/wp_ar2017_v5FINAL_WEBlr.pdf.

Be the first to comment on "No. 5 – Corporate charitable giving is not likely to affect operations budgets at Patterson Park"